Timely & Relevant News: Markets Grapple With Tariffs & Uncertainty

History and Henry Poulsen have taught us to, "Be pragmatic enough to change plans when facts and circumstances warrant." As a result of the significant developments over the last several days, we are currently taking a more conservative posture in our actively managed models.

Recent Market Performance

Equity markets have been experiencing heightened volatility and have rattled investor sentiment. The volatility has been driven by ongoing uncertainties surrounding tariffs and now the threat of retaliatory and reciprocal tariffs.

Retaliatory tariffs are imposed by one country in response to tariffs by another country placed on their exports. In the current situation, the U.S. threatened to implement a 25% tariff on Canadian imports, prompting Canada to retaliate with threats of their own 25% tariff on U.S. goods, including energy exports to key states. In turn, the U.S. has threatened to respond with reciprocal tariffs, further escalating trade tensions between the two nations. This back-and-forth tariff cycle increases economic uncertainty and market volatility, which impacts consumer and business confidence and related spending.

Tariff Uncertainty's Role in the Downturn

A key factor behind the recent market selloff is the uncertainty surrounding trade tariffs and their economic implications. The lack of clarity regarding tariff policies has made it difficult for markets to stage a meaningful recovery, as investors hesitate to make significant moves without a clearer outlook. This week will bring an array of economic data, including Job Openings and Labor Turnover Survey (JOLTS) job openings, consumer and wholesale inflation, on top of ongoing government funding negotiations, which all have the potential to influence the market.

Uncertainty Moves Yields and Volatility

The ambiguity that is contributing to the equity market pullback is also sending bond yields lower and bond prices higher, a phenomenon otherwise known as "flight to safety." Recent remarks from Treasury Secretary Scott Bessent, alluded to a potential “detox period” for an economy that had become dependent on government spending. This statement intensified the sell-off as bearish investors pointed to weakening growth forecasts. As the equity market declines, increased bond buying pushes bond prices higher - underscoring the value of owning bonds in times of market volatility.

The Bottoming Process

A broader market recovery is not expected to begin until there is greater clarity on tariffs and trade relationships. This process could take months rather than weeks as markets adjust expectations for economic growth and corporate profits. Presently, there is limited technical evidence supporting a "buy-the-dip" strategy, warranting caution. Last week, broader market indexes fell by 3.1%, with threats of new tariffs on Canada, China, and Mexico that were scheduled to take effect on March 4. The S&P 500 recently broke through critical support levels near its October lows (5,703) and breached its 200-day moving average (dma) (5,733), suggesting the drawdown may have more room to run.

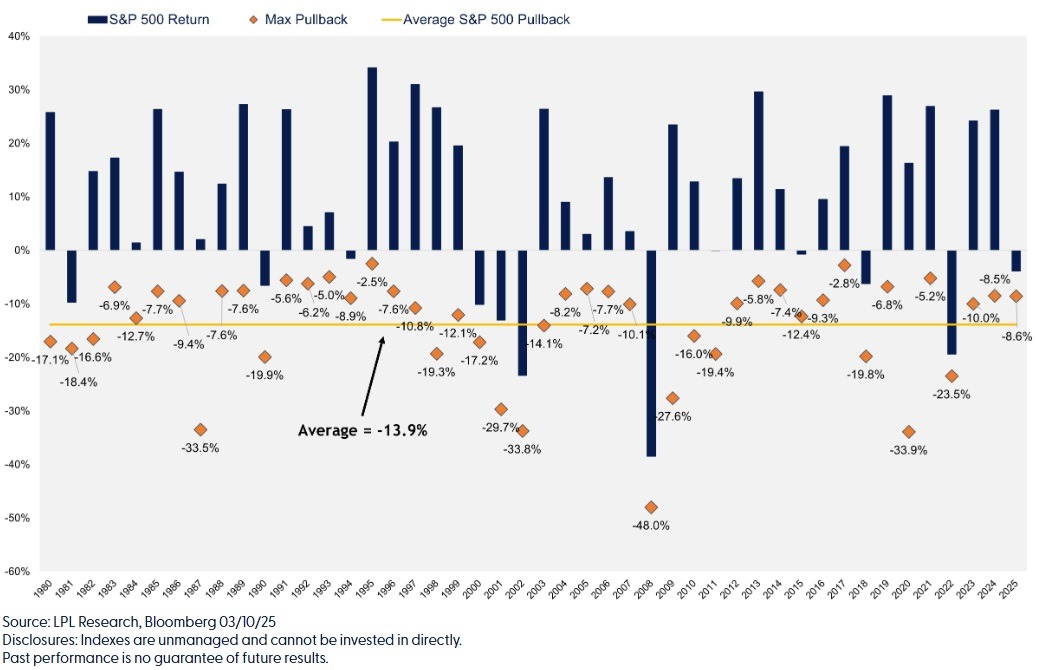

Understanding Market Corrections

Historically – and for a variety of different reasons - the S&P 500 typically undergoes three corrections of 5% annually, a 10% drop once a year, a 15% drop every two years, and a bear market of 20% or more every three years. The average S&P 500 maximum drawdown for a given year is 13.9%, while the average gain during that period (since 1980) has been 11.9%, providing evidence that market volatility is like a toll investors pay on the road to attractive long-term returns. The S&P 500 max pull down can be described as the largest peak-to-trough decline in the index over a specific period. It measures how much the S&P 500 has dropped from its highest point to its lowest point before recovering.

What Happens Next?

We are expecting that volatility and uncertainty will continue. We are currently taking a more conservative posture in our actively managed models, while paying close attention to market signals in an effort to make wise and appropriate choices that align with our client's investment objectives.

If you have specific questions or would like to discuss your own investment strategy or financial planning needs, we welcome you to call us at 302.234.5655 or email us at contactus@covenantwealthstrategies.com to set up time to discuss further.

Disclosures:

All indexes are unmanaged and cannot be invested into directly. Past performance is no guarantee of future results.

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities. All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

This Research material was prepared by LPL Financial, LLC, FactSet.