Planning For 2026: Retirement Plans & HSA Contribution Limits

December 18, 2025

It's always a good time to plan for your financial future. As the upcoming new year approaches, it provides a good reason to consider the new contribution limits for retirement plans and health savings accounts (HSAs) in 2026.

Retirement Plan Contributions

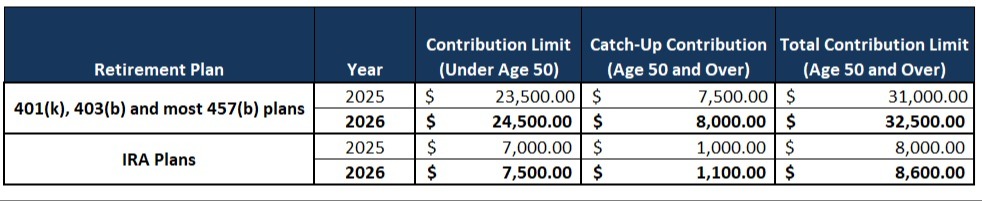

The IRS recently announced that beginning in 2026, taxpayers will be allowed to contribute an additional $1,000 into their 401(k), 403(b) and most 457(b) plans. The 2026 contribution limit for these retirement plans will increase from the current level of $23,500 to $24,500.

Individuals age 50 and above are also eligible for catch-up contributions to their 401(k), 403(b) and most 457(b) plans. This means that these individuals can contribute above the $24,500 limit. The 2026 catch-up contribution limit has increased to $8,000. In total, employees age 50 and above can contribute up to $32,500 into these retirement plans.

Additionally, individuals between the ages of 60 to 63 can make enhanced catch-up contributions of up to $11,250 to their 401(k), 403(b) and most 457(b) plans, bringing the total potential contribution to $35,750. The enhanced catch-up contributions are in place of the catch-up contributions described in the paragraph above. We encourage you to speak with your advisor to discuss your specific goals and strategy.

The limits for IRA/Roth-IRA contributions in 2026 has increased (up to $7,500 per year). The IRA /Roth IRA catch-up contributions for individuals age 50 and above has also increased to $1,100. In total, employees age 50 and above can contribute up to $8,600 in their IRAs/Roth-IRAs. There is no enhanced catch-up contribution for IRAs and Roth IRAs.

Additionally, recent legislation has also made changes to HSAs contribution limits in 2026. Below are several of the important highlights to note.

Higher Health Savings Account (HSA) Limits In 2026

Individuals

- In 2026, the maximum annual contribution amount is $4,400 for an individual (up from $4,300 in 2025).

- The catch-up contribution amount for those age 55 and over is $1,000 per year.

Families:

- For families, the maximum annual contribution amount is $8,750 per year in 2026 (up from $8,550 in 2025).

- If a spouse is age 55+, a catch-up contribution of $1,000 can be made, however the contribution must be in a separate account for each spouse who qualifies.

- For a family in the 35% marginal tax bracket, a maximum contribution can result in a federal income tax savings of nearly $3,000 plus any state income tax and other benefits.

Almost anyone enrolled in a high deductible health plan that is HSA-qualified can set-up an HSA and benefit from the tax advantage. HSAs are an increasingly popular tax-favored benefit for workers and their families.

While there are many pages to the tax code, these are some of the ways that you and your family can benefit in 2026 to potentially reduce your tax bill. We are more than happy to collaborate with you and your tax advisor on planning strategies for 2026.

If you have questions about your specific financial planning or investment strategy needs, we welcome you to Contact Us to set up time to discuss further.

Disclosures:

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. This information is not intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax situation with a qualified tax advisor.

https://www.irs.gov/newsroom/401k-limit-increases-to-24500-for-2026-ira-limit-increases-to-7500