National 529 Day - Planning Ahead For The Next Generation

As the cost of education continues to rise, proactive planning remains one of the most meaningful gifts that families can provide to the next generation. Preparing early can help create greater flexibility and confidence when future educational opportunities arise.

May 29th is recognized as National 529 College Savings Day — a reminder of the value and flexibility 529 plans can offer when preparing for future education expenses.

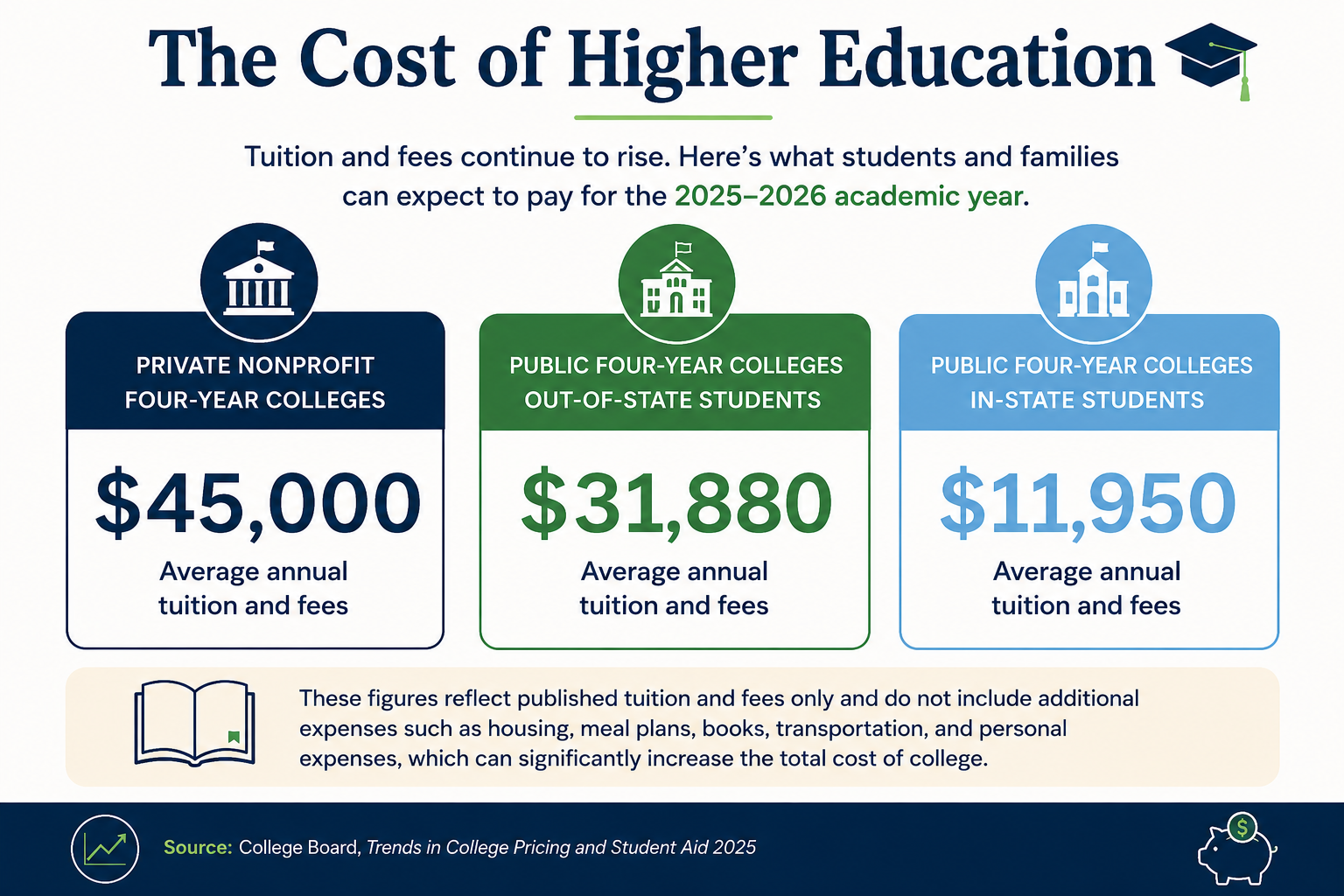

For the 2025–2026 academic year, the average published tuition and fees reached approximately $45,000 at private nonprofit colleges, while out-of-state students attending public universities are paying an average of $31,880 annually. In-state students at public universities continue to pay less on average, though costs have still climbed to roughly $11,950 per year, according to the College Board Trends in College Pricing and Student Aid 2025 Report. These figures do not include additional expenses such as housing, meal plans, books, transportation, and other day-to-day costs that can significantly increase the overall investment in higher education.

It is no surprise that many families feel unprepared for the rising cost of higher education. According to recent research highlighted by Morningstar, more than one-third of parents with young children expect to save $25,000 or less for future education costs, which is well below the projected cost of a four-year degree. At the same time, the College Board’s 2025 Trends in Student Aid report revealed that parents and students borrowed more than $102 billion in federal and private loans during the 2024–2025 academic year alone, underscoring the continued financial pressure many families face when planning for college expenses.

Our team at Covenant Wealth Strategies prioritizes helping families prepare by providing education planning through a variety of tax-favored strategies. Additionally, we seek to provide strategies to also save on the cost of college.

If you are wondering if a 529 could fit your planning needs, we've compiled a list of common 529 Plan questions below.

Why are 529 Plans a good option?

529 Plans allow you to increase savings for a loved one's education expenses. A benefit of using a 529 Plan is that it provides tax-deferred growth and tax-free withdrawals. In addition to the benefit of potential compounded growth, it also gives contributors control over the assets, so children can’t use the funds for a purpose other than education.

What types of education can 529 Plans fund?

While 529 Plans can be used for four-year colleges, they can also be used to cover the costs of vocational school, community college, some foreign institutions, and even qualified kindergarten through 12th grade tuition.

Who can fund a 529 Plan?

Anyone! Common contributors include parents, grandparents, or other relatives. However, really anyone who wants to support a loved one’s future education can open and fund a 529 Plan. The annual gift tax exclusion is $19,000 per recipient. For married couples electing to split gifts, the exclusion doubles to $38,000 per beneficiary with gift tax reporting requirements.

What happens if the child ends up not needing the funds?

If the child doesn’t need the funds anymore – say they get a scholarship, or decide not to go to college – the 529 Plan can flex to fit their needs. You can typically transfer the money to another eligible family member without tax consequences. Plus, you can use the funds for other education-related expenses – not just tuition. So if the child receives a grant or other financial aid that covers most or all of tuition, you can apply the 529 funds to other expenses, including:

- Fees, books, supplies and equipment

- Room and board for beneficiaries attending on at least a half-time basis

- Computer technology, equipment, and internet access

- Apprenticeship expenses

- Up to $10,000 for student loan repayment

Did you know that qualifying 529 funds can also be used to fund a Roth IRA for beneficiaries?

If college might be in the future plans for your child or grandchild, we encourage you to check out our College Planning Resource Page, and Contact Us so we can help you prepare for the future and design "Strategies for Your Success".

Source:

https://research.collegeboard.org/media/pdf/Trends-in-College-Pricing-and-Student-Aid-2025-final_1.pdf?utm_source=chatgpt.com

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. Prior to investing in a 529 Plan, investors should consider whether the investor's or designated beneficiary's home state offers any state tax or other state benefits such as financial aid, scholarship funds, and protection from creditors that are only available for investments in such state's qualified tuition program. Withdrawals used for qualified expenses are federally tax free. Tax treatment at the state level may vary. Please consult with your tax advisor before investing.