Market Volatility & Economic Update

August 6, 2024

The recent market decline has reignited discussions about the potential for a recession. As investors reacted to global uncertainties and a mix of economic data, the overall market sentiment shifted towards caution. The sharp decline in equities reflects growing worries about global conflict and slowing economic growth as well as a rather complicated concept known as “carry trade”. Many market participants are now questioning whether this downturn is a temporary correction or a sign of deeper economic challenges ahead.

International Conflict

Escalating tensions in the Middle East are significantly impacting global markets. Concerns over broader geopolitical instability led to heightened market volatility. Investors reacted to fears that the conflict could escalate further. The heightened uncertainty has led investors to adopt a more cautious approach.

Labor Market

The latest snapshot of the labor market is consistent with a slowdown, and we have warning signs suggesting more weakness.

The U.S. jobs report for July 2024 showed a notable slowdown in job growth, with only 114,000 jobs added, significantly below expectations. The unemployment rate rose to 4.3%, the highest in nearly three years, up from 4.1% in June. This unexpected increase in unemployment has raised questions about the labor market. There are some who believe that this data was temporarily impacted and distorted by job losses related to recent hurricane Beryl.

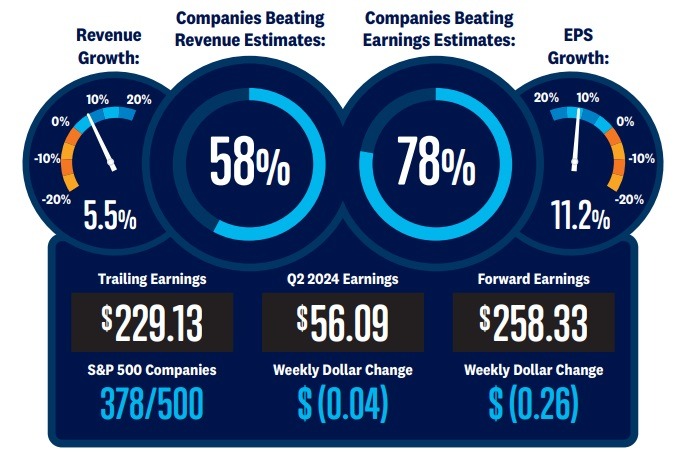

Earnings

Despite emerging weaknesses in the labor market, Q2 earnings have been strong, with about 75% of S&P 500 companies reporting positive results. Earnings per share (EPS) growth for the S&P 500 is tracking to 11% year over year. The average upside surprise of 4.6% is slightly below recent quarterly trends. Healthcare, utilities, and financials have produced the biggest average upside surprises. Industrials, consumer staples, and real estate have produced the least upside. Technology, financials, and comm services are contributing most to growth. Forward estimates for the S&P 500 held firm over the past week and impressively sit just 0.6% below July 1 levels, a solid result relative to historical average declines near 2%. The S&P 500’s forward price-to-earnings ratio has edged lower toward 20.

Earnings are an essential component in determining the overall health of the economy and recessions. The generally accepted definition of a recession is 2 consecutive quarters of negative GDP. The National Bureau of Economic Research (NBER) is responsible for analyzing the data and making official recession calls. It should be noted that the most recent GDP report showed an annualized 2.8% GDP for the second quarter – which is relatively strong and represents an increase from the first quarter GDP of 1.4%.

The Fed

As anticipated, the Federal Reserve did not cut interest rates last week. After the release of the July labor report, there were concerns that the Fed might be late in lowering rates, just as it was slow to raise them. The Fed noted that while inflation has decreased over the past year, it remains somewhat elevated. Additionally, job gains have slowed, and the unemployment rate has risen yet remains relatively low. The Fed stated that it won't consider rate cuts until inflation is consistently moving towards 2%. The next meeting is in mid-September, with the decision likely to be viewed through a political lens.

What Happens Next?

The market is currently pricing in the equivalent of 4.5 interest rate cuts by the end of the year, with the first likely being a 0.50% reduction at the September 18th FOMC meeting or earlier.

Historically, the S&P 500 typically undergoes three corrections of 5% annually, a 10% drop once a year, a 15% drop every two years, and a bear market of 20% or more every three years. We view the current market correction as an overreaction to slowing economic data, suggesting the Fed may be delayed in cutting rates. This pullback may presents potential buying opportunities for long-term investors.

If you have specific questions or would like to discuss your own investment strategy or financial planning needs, we welcome you to call us at 302.234.5655 or email us at contactus@covenantwealthstrategies.com to set up time to discuss further.

Disclosures:

All indexes are unmanaged and cannot be invested into directly. Past performance is no guarantee of future results.

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities. All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

This Research material was prepared by LPL Financial, LLC, FactSet 8/02/24.